Cross-Border Agentic Commerce: How AI Agents Solve the Localization, Currency, and Compliance Problem

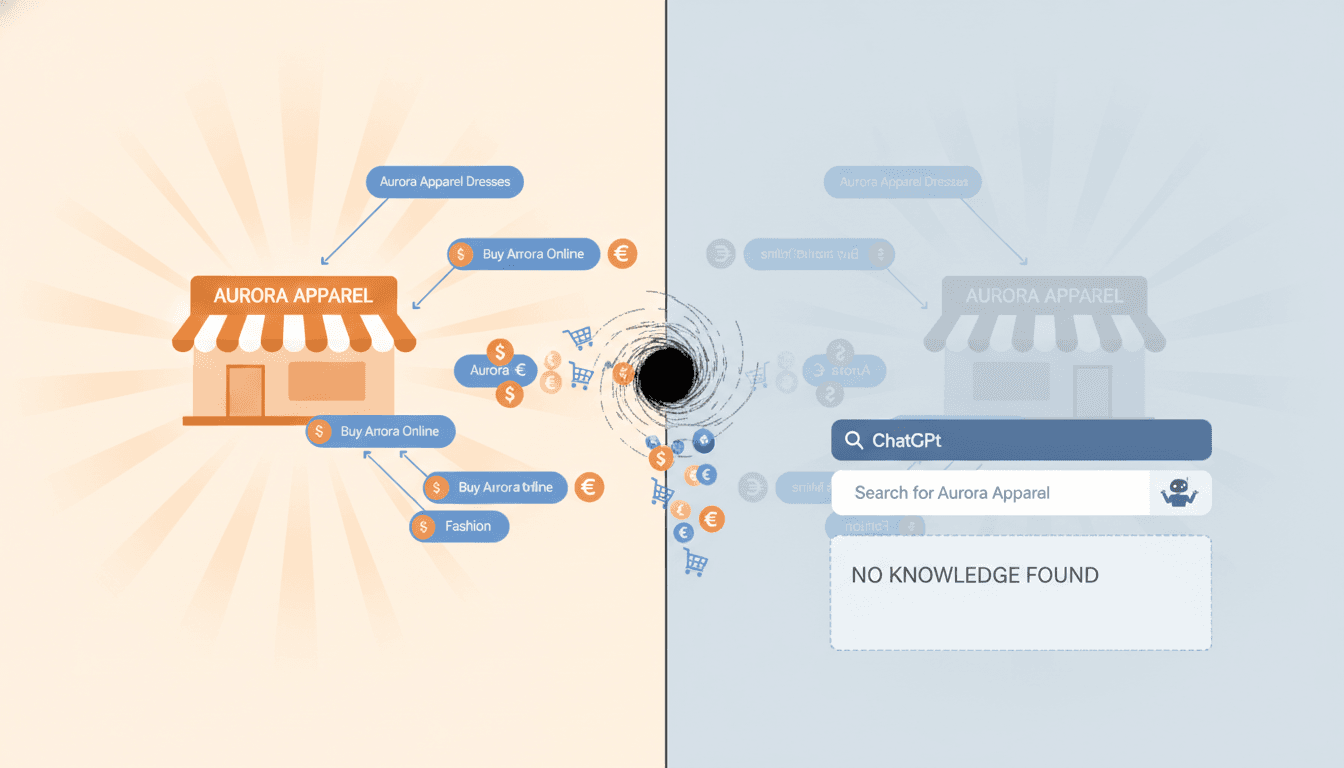

Ninety-two percent of global shoppers prefer websites that display prices in their local currency. That single statistic explains why cross-border commerce remains one of the highest-friction, highest-opportunity segments in retail. With global cross-border ecommerce sales projected to reach $1.2 tr

Cross-Border Agentic Commerce: How AI Agents Solve the Localization, Currency, and Compliance Problem

Last updated: March 2026

Ninety-two percent of global shoppers prefer websites that display prices in their local currency. That single statistic explains why cross-border commerce remains one of the highest-friction, highest-opportunity segments in retail. With global cross-border ecommerce sales projected to reach $1.2 trillion by 2026 and agentic commerce expected to drive over $190 billion in ecommerce revenue by 2030, a new class of AI-powered agents is emerging to handle what human teams and static rule engines never could: real-time currency conversion, multilingual customer engagement, customs classification, regulatory compliance, and local payment method selection – all autonomously, all simultaneously, across every market a brand enters.

This is cross-border agentic commerce. And for international commerce managers watching margins erode under tariff complexity, payment fragmentation, and localization costs, it represents the most consequential operational shift since marketplace aggregation.

The Cross-Border Challenges AI Agents Are Built to Solve

Expanding internationally has always meant wrestling with three interrelated problems: currency, language, and regulations. Traditional approaches – hiring local teams, maintaining static translation databases, contracting compliance consultants per market – scale linearly with cost and headcount. Agentic AI changes the economics entirely.

Currency and Pricing

AI agents handle live foreign exchange rate conversion for prices, shipping costs, taxes, and discounts simultaneously. Rather than displaying a single base currency with a conversion disclaimer, agents dynamically render localized pricing that accounts for regional purchasing power, preferred payment authentication methods, and cultural expectations around pricing display (tax-inclusive in Europe, tax-exclusive in the United States, installment-first in Brazil).

Machine learning algorithms analyze local payment behaviors to optimize checkout flows per market. The result: regional personalization – encompassing currency display, language, and trust signals – can increase conversion rates by 25 to 30 percent in new geographic markets, according to multiple cross-border commerce benchmarks.

Language and Cultural Nuance

The global natural language processing market is projected to reach $35.1 billion by 2026, and modern multilingual AI agents go well beyond word-for-word translation. They detect language, respond in cultural context, handle idiomatic nuances, and maintain conversation state across languages within a single interaction.

For cross-border commerce, this means AI agents can translate product listings, customer support conversations, and marketing assets into local languages and cultural tones automatically. Supply chain communication benefits equally: AI bridges language gaps within multinational logistics networks through advanced NLP, enabling accurate cross-language coordination for customs documentation, carrier instructions, and returns processing.

Regulations and Trade Compliance

Only one-third of businesses have applied AI to inventory management, cross-border logistics, or compliance – the areas most responsible for cost overruns and delivery failures. The gap is enormous, and the cost of inaction is rising. A single product misclassification under shifting tariff regimes can result in hundreds of thousands of dollars in back duties and penalties.

AI-Driven Regional Personalization

The 25 to 30 percent conversion increase from regional personalization is not a theoretical projection. It reflects what happens when every element of the shopping experience – price display, payment options, language, trust signals, shipping estimates, return policies – adapts to the buyer’s location in real time.

AI agents make this operationally viable at scale. Instead of maintaining separate storefronts or localized checkout flows per market, a single agentic system dynamically adjusts the experience based on buyer context. In Brazil, the agent presents PIX as the primary payment option and displays installment pricing. In India, UPI appears first. In Germany, prices include VAT and the interface renders in formal German. In Japan, the agent adjusts for local address formatting and delivery window expectations.

The key distinction from traditional localization platforms: agentic systems reason and improve continuously. They do not rely on static configuration files or manual market-by-market setup. They observe conversion patterns per region and adjust autonomously.

Customs and Duties Automation

Tariff complexity has worsened dramatically in 2026. Five defining issues dominate the landscape: supercharged enforcement through False Claims Act suits and criminal prosecutions, expanded forced labor import regimes, proliferation of Section 232 duties, the USMCA six-year review, and landmark IEEPA tariff rulings. AI-targeted audits are now a reality – customs authorities use their own algorithms to flag suspicious classifications.

Agentic AI platforms automate compliance workflows that previously consumed thousands of broker hours per year. Unlike rule-based automation, these systems reason across trade classification data, monitor global policy changes without manual prompting, and validate declarations against live regulatory databases before customs submission.

For brands, the practical impact is landed cost transparency. AI agents can pre-calculate duties, taxes, and import fees during the purchase conversation – before the buyer confirms the order. This eliminates the post-purchase surprise that drives cross-border cart abandonment and chargeback disputes. The agent handles HS code classification, de minimis threshold evaluation, trade agreement eligibility, and restricted party screening in the background, surfacing only the final landed cost to the consumer.

Payment Method Fragmentation

Payment fragmentation is the silent conversion killer in cross-border commerce. Cards dominate in North America and parts of Europe. PIX processes the majority of digital payments in Brazil. UPI handles over 18 billion transactions per month in India. Mobile money leads in much of Sub-Saharan Africa. QR-based systems, bank transfers, and buy-now-pay-later schemes each command significant share in their respective markets.

AI agents must dynamically route payments through the optimal processor and method per market – a capability known as payment orchestration. The agent evaluates the buyer’s location, the available payment infrastructure, transaction costs, and settlement timing to select the best payment path automatically.

How AP2 and UCP Address Fragmentation

Two emerging protocols aim to prevent the payment layer from becoming the bottleneck for agentic commerce. The AP2 standard (Agentic Payments Protocol) creates machine-friendly, policy-controlled payment authorization that works at API speed, enabling agents from different providers to transact through a common interface. Google’s Universal Commerce Protocol (UCP), launched in January 2026, requires cryptographic proof of user consent for each transaction, establishing a trust layer that payment networks and regulators can verify independently.

The underlying concern is real: merchants and banks will not scale support for agentic transactions if every agent framework invents its own payment authorization logic. AP2 and UCP represent the industry’s attempt to create shared rails before fragmentation becomes entrenched.

UPI-ChatGPT: The Largest Live Agentic Payment Deployment

India’s integration of UPI with ChatGPT represents the most concrete high-scale agentic payment deployment currently operational. With UPI processing over 18 billion transactions per month across India’s digital economy, the integration allows AI agents to initiate and complete payments through the country’s real-time payment infrastructure within a conversational interface.

This deployment matters for cross-border commerce managers because it demonstrates agentic payments operating at population scale – not as a pilot or proof of concept, but as production infrastructure handling real transaction volume. It also illustrates a regulatory reality: India has moved faster than any other major economy in enabling AI-initiated payments while simultaneously proposing consumer protections. A bill amending the Consumer Protection Act would expand the definition of “unfair trade practices” to include undisclosed terms, fees, dynamic pricing, and algorithmic influence on consumer behavior – directly applicable to AI agents making purchasing decisions.

The UPI-ChatGPT model is likely a template for other markets. Brands operating cross-border should watch for similar integrations with PIX in Brazil, FPS in the United Kingdom, and SEPA Instant in the European Union.

Regulatory Divergence Across Major Markets

No jurisdiction has enacted regulation specifically addressing agentic commerce as of March 2026. Organizations must navigate a patchwork of existing laws – consumer protection, data privacy, product liability, agency law – none of which were designed for autonomous purchasing agents.

European Union

The EU AI Act is the most ambitious regulatory response, but it predates mainstream agentic commerce and contains no specific provisions for autonomous purchasing agents. High-risk AI system rules take effect in August 2026, and agentic commerce systems that influence financial decisions or handle sensitive data are likely to be classified as high-risk. Penalties reach up to 35 million EUR or 7 percent of global annual revenue, whichever is higher. The first major AI Act penalty was issued in March 2026: a 35 million EUR fine against a major ecommerce platform for insufficient algorithmic transparency.

The revised Product Liability Directive extends strict liability to software and AI, treating defective AI like a defective physical product – the most significant near-term legal risk for AI commerce providers operating in the EU.

United States

The federal approach remains fragmented. The FTC has signaled reduced appetite for AI-specific regulation, preferring to target bad actors rather than the technology itself through existing Section 5 authority. Multiple state AI laws took effect on January 1, 2026, but a December 2025 Executive Order proposes federal preemption of inconsistent state laws. Texas TRAIGA, effective January 1, 2026, establishes a regulatory framework focusing on transparency, risk management, and consumer protection for high-risk AI systems, including a regulatory sandbox.

China

New rules on internet platform pricing behavior take effect in April 2026. These rules prohibit operators from imposing unreasonable conditions and ban price discrimination using data, algorithms, or platform rules – directly relevant to AI agents that dynamically adjust pricing or product recommendations based on user data.

India

Beyond the UPI-ChatGPT deployment, India is actively expanding consumer protections. The proposed amendments to the Consumer Protection Act would cover undisclosed fees, dynamic pricing, and algorithmic influence on purchasing decisions. The LGPD-equivalent data protection framework adds rights to explanation, non-discrimination, and human review for automated decisions.

The Critical Legal Gaps

Three questions remain unanswered across all jurisdictions. First, data consent and authority: can AI agents process personal data and execute purchases without explicit human approval per transaction? Second, contract formation liability: who bears responsibility when an AI agent makes an erroneous purchase – the consumer, the AI provider, the merchant, or the platform? Third, security: with a reported 25 percent vulnerability rate in AI agent manipulation, how should fraud liability be allocated?

Protocol Fragmentation Risk

The proliferation of competing standards creates a real risk for brands building cross-border agentic infrastructure. At least six major protocols are now active or piloting:

- Mastercard Agent Pay: Live since 2025, applies Model Context Protocol to Secure Remote Commerce for agent verification and data exchange.

- Visa Trusted Agent Protocol: Piloting in 2026 with Asia Pacific markets, an open framework to distinguish legitimate AI agents from malicious bots.

- OpenAI Agentic Commerce Protocol (ACP): Standard for AI agent-merchant interactions, aligned with Visa’s framework.

- Google Universal Commerce Protocol (UCP): Launched January 2026, requires cryptographic consent proof per transaction.

- Coinbase x402: HTTP-native, crypto-aligned payment protocol for AI agent transactions.

- Cloudflare Web Bot Auth: The underlying infrastructure supporting both Visa and Mastercard frameworks, built in collaboration with Shopify, Checkout.com, Worldpay, and Adyen.

The fragmentation risk is concrete: merchants who support one protocol but not another become invisible to agents running on the excluded stack. Fiserv has adopted protocols from both Visa and Mastercard. PayPal partnered with Mastercard in October 2025 to accelerate secure global agentic commerce. eBay has taken the opposite approach, prohibiting agentic bots entirely in its user agreements.

For cross-border brands, the strategic imperative is protocol optionality – supporting multiple standards while the market consolidates, rather than betting on a single winner.

Implementation Guide for Cross-Border Brands

Brands preparing for cross-border agentic commerce should prioritize the following steps, organized by urgency.

Immediate Actions

-

Audit payment method coverage by market. Map every target market to its dominant payment methods (cards, PIX, UPI, mobile money, bank transfers) and verify your payment stack supports agent-initiated transactions through each.

-

Implement AI-powered customs classification. Connect your product catalog to an agentic compliance platform that handles HS code assignment, de minimis evaluation, and landed cost calculation in real time. This eliminates the post-purchase duty surprise that drives cross-border returns.

-

Deploy multilingual AI agents. Move beyond static translation to conversational AI that adapts language, tone, and cultural context per market. Prioritize markets where WhatsApp or messaging-based commerce dominates, as conversational AI delivers the highest ROI in these channels.

-

Update contracts and terms of service. Add explicit agentic AI clauses to vendor agreements, customer terms, and insurance policies covering unauthorized purchases, agent errors, and agent-to-agent transactions.

Before August 2026

-

Assess EU AI Act high-risk classification. If your AI system influences financial decisions, handles sensitive consumer data, or operates in EU markets, complete the required risk assessment and technical documentation before the August 2026 enforcement deadline.

-

Implement consent verification. Adopt cryptographic or verifiable proof of user authorization per transaction, aligned with Google’s UCP and Mastercard’s Verifiable Intent frameworks.

-

Build audit trail infrastructure. Log every agent decision, tool call, data access event, and outcome. GDPR, LGPD, and the EU AI Act all require demonstrable record-keeping for automated systems.

Ongoing

-

Monitor protocol convergence. Track Mastercard Agent Pay, Visa Trusted Agent Protocol, and UCP adoption rates. Aim for multi-protocol support rather than single-standard commitment.

-

Track regulatory developments quarterly. The landscape is shifting fast – Brazil’s Bill 2338/2023, China’s April 2026 pricing rules, India’s consumer protection amendments, and U.S. federal preemption each have the potential to reshape compliance requirements.

Frequently Asked Questions

What is cross-border agentic commerce?

Cross-border agentic commerce refers to AI-powered agents that autonomously handle the end-to-end complexity of international transactions – including currency conversion, language translation, customs classification, regulatory compliance, and local payment method selection – on behalf of consumers or businesses. Unlike traditional automation, these agents reason, adapt, and improve continuously across markets.

How do AI agents handle currency conversion in real time?

AI agents connect to live foreign exchange rate feeds and dynamically calculate localized pricing that includes product cost, shipping, taxes, duties, and applicable discounts in the buyer’s local currency. Machine learning models further optimize pricing display based on regional conventions (tax-inclusive vs. tax-exclusive, installment-first vs. total-first) to maximize conversion.

Which regulations should cross-border brands prepare for in 2026?

The most impactful near-term regulations include the EU AI Act high-risk system rules (August 2026), China’s internet platform pricing rules (April 2026), India’s Consumer Protection Act amendments, and Brazil’s Bill 2338/2023. In the United States, brands should monitor the tension between state AI laws and proposed federal preemption. The EU’s revised Product Liability Directive, which extends strict liability to software and AI, represents the single largest legal risk for AI commerce providers.

What is the difference between ACP, UCP, and TAP?

The Agentic Commerce Protocol (ACP), developed by OpenAI, standardizes how AI agents interact with merchants. Google’s Universal Commerce Protocol (UCP) focuses on cryptographic proof of user consent per transaction. Visa’s Trusted Agent Protocol (TAP) is an open framework for verifying that an AI agent is legitimate rather than a malicious bot. These protocols address different layers of the same problem – agent-merchant interaction, consent verification, and identity trust – and are likely to coexist or converge rather than compete directly.

How does UPI-ChatGPT work as an agentic payment system?

India’s UPI infrastructure, which processes over 18 billion transactions per month, has been integrated with ChatGPT to allow AI agents to initiate and complete payments within a conversational interface. Users authorize transactions through UPI’s existing authentication layer while the AI agent handles product discovery, comparison, and purchase orchestration. It is the largest live deployment of agentic payments globally and serves as a reference architecture for similar integrations in other real-time payment networks.

What happens if an AI agent makes an unauthorized cross-border purchase?

Under most existing legal frameworks, the deploying organization bears primary liability. Courts and regulators treat the business that deployed the AI agent as the party best positioned to prevent harm. However, the EU’s revised Product Liability Directive could shift liability to the AI developer or producer under strict liability principles. Contract law analysis examines whether binding consent existed at the time of purchase. This is an evolving area – organizations should update their terms of service and insurance coverage to address agentic-specific scenarios explicitly.

How can brands avoid becoming invisible to AI agents due to protocol fragmentation?

Support multiple agentic commerce protocols rather than committing to a single standard. Ensure your payment infrastructure is compatible with Mastercard Agent Pay and Visa Trusted Agent Protocol at minimum, and monitor UCP and ACP adoption. Work with payment orchestration platforms that abstract protocol differences, so your products and checkout flows remain discoverable regardless of which agent framework a consumer uses.

This article is for informational purposes only and does not constitute legal or regulatory advice. Organizations should consult qualified legal counsel for jurisdiction-specific compliance guidance.

Hexagon Team

Published March 8, 2026